Introducing the Prime Minister Apna Ghar Program: Ghar Hoto Apna

The Prime Minister Apna Ghar Program, under the evocative title “Ghar Hoto Apna,” represents a significant federal government initiative aimed at revolutionizing affordable housing finance. This comprehensive Markup Subsidy and Risk Sharing Scheme has been meticulously designed to empower citizens, particularly first-time homeowners, to realize their dream of owning a residence. It addresses a critical societal need, providing accessible financial pathways for acquiring or constructing homes.

The program’s introduction signals a strong commitment from the government to bolster the housing sector and improve living standards across the nation. Through a structured framework, it seeks to ease the financial burden associated with homeownership, making it a tangible reality for a wider segment of the population. This forms a core component of the government’s broader socio-economic development agenda.

آنلائن اپلائی کے لیے یہاں کلک کریں

Click Here to Apply Online

The Vision Behind the Apna Ghar Program for Affordable Housing

At its heart, the Apna Ghar Program endeavors to bridge the existing housing deficit by offering subsidized financing options. The government recognizes that prohibitive costs often deter individuals from purchasing homes, leading to widespread demand for affordable solutions. This scheme directly tackles this challenge by significantly reducing the loan’s effective markup for beneficiaries.

Its strategic design aims to stimulate economic activity within the construction sector, creating jobs and fostering growth in allied industries. By making housing loans more attainable, the program contributes not only to individual welfare but also to national economic prosperity, marking a pivotal step towards a more equitable society. NewSchemes.com provides further details on such government initiatives.

Key Features of the Ghar Hoto Apna Scheme

The Ghar Hoto Apna scheme is distinguished by several attractive features, making it a compelling option for prospective homeowners. It is designed to cover various housing needs, including the direct purchase of houses and flats, construction of new homes on already owned land, or even the purchase of a plot followed by construction. This flexibility ensures a broad reach within the target demographic.

Beneficiaries can apply for loans to acquire housing units up to 10 Marla or 2,720 sq. ft. for a house, and up to 1500 sq. ft. for a flat. This generous sizing allows for diverse housing preferences to be accommodated. The maximum loan size available under this program is an impressive PKR 10 million, providing substantial financial support for home acquisition.

One of the most appealing aspects of the Apna Ghar Program is its innovative financial structure. Loans are available for a generous tenor of up to 20 years, with the federal government offering a substantial markup subsidy for the first 10 years of the loan term. This arrangement significantly reduces the initial financial strain on borrowers.

End-users will benefit from a fixed markup rate of just 5 percent, paid directly by the customer. In contrast, the bank’s pricing is set at one-year KIBOR plus 3 percent, with the government covering the difference through its subsidy. Crucially, the scheme stipulates that no processing costs or prepayment penalties will be charged to customers, simplifying the loan process and promoting financial transparency.

Furthermore, loans will be provided on a favorable 90:10 Loan-to-Value (LTV) ratio, meaning borrowers need to contribute only 10 percent equity, while the loan covers the remaining 90 percent. To mitigate risks for financial institutions, the government will also provide risk coverage of 10 percent of the outstanding portfolio on a first-loss basis, encouraging banks to participate actively in this vital Apna Ghar Program.

Eligibility for the Wazir-e-Azam Apna Ghar Program

The Wazir-e-Azam Apna Ghar Program is specifically tailored for first-time homeowners who are citizens of Pakistan and hold valid CNICs. A primary criterion is that applicants must not own any other housing unit in their name, ensuring that the benefits reach those who genuinely need a primary residence. This focus helps in equitable distribution of resources.

Participating Financial Institutions in the Apna Ghar Program

To ensure widespread accessibility for the Apna Ghar Program, a consortium of financial institutions has been designated as Participating Financial Institutions (PFIs). This includes all commercial banks, Islamic banks, Microfinance Banks (MFBs), and the House Building Finance Company Limited (HBFCL). Their collective involvement ensures that potential beneficiaries have multiple avenues to apply for this beneficial scheme.

Accessing the Apna Ghar Program: Application Process

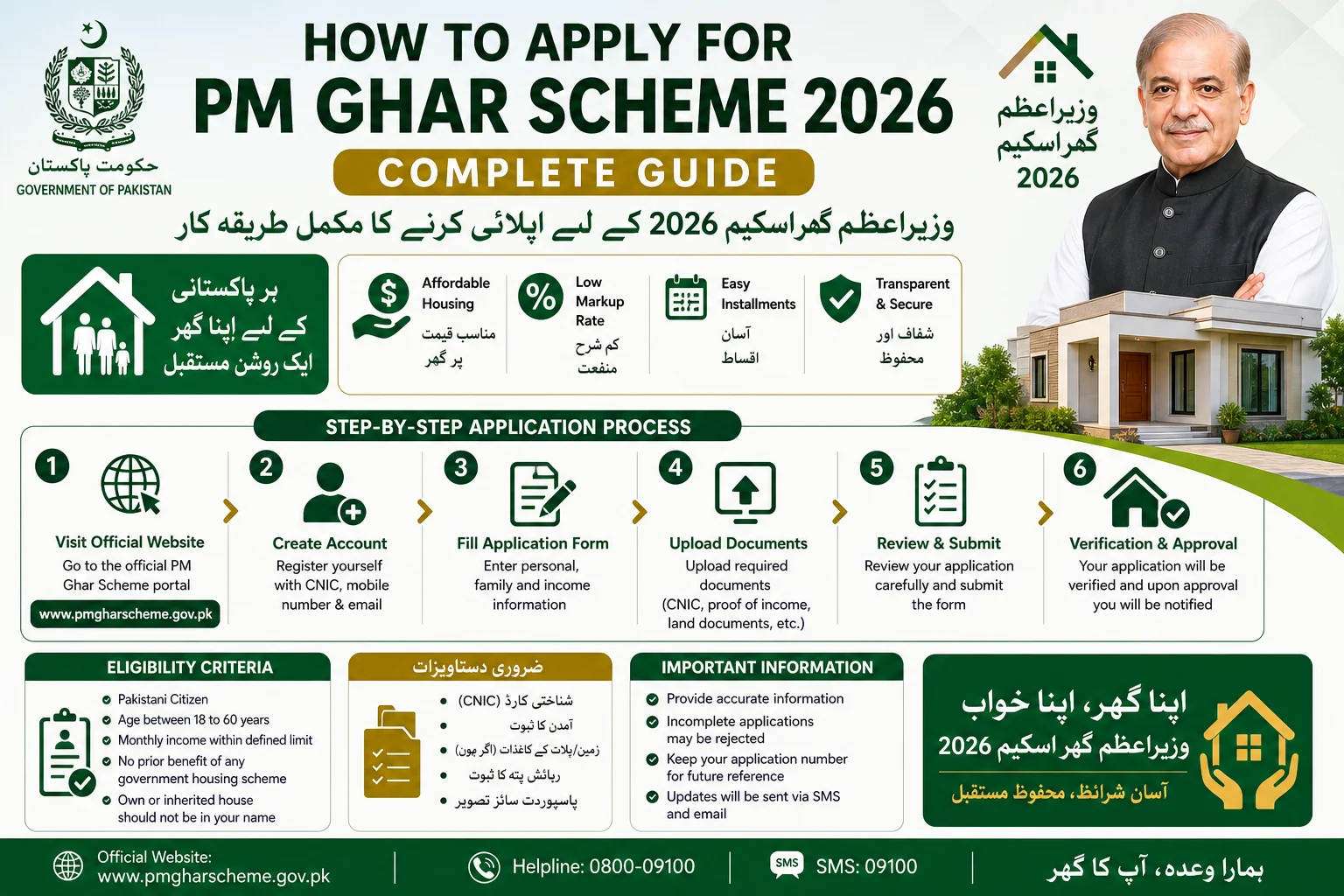

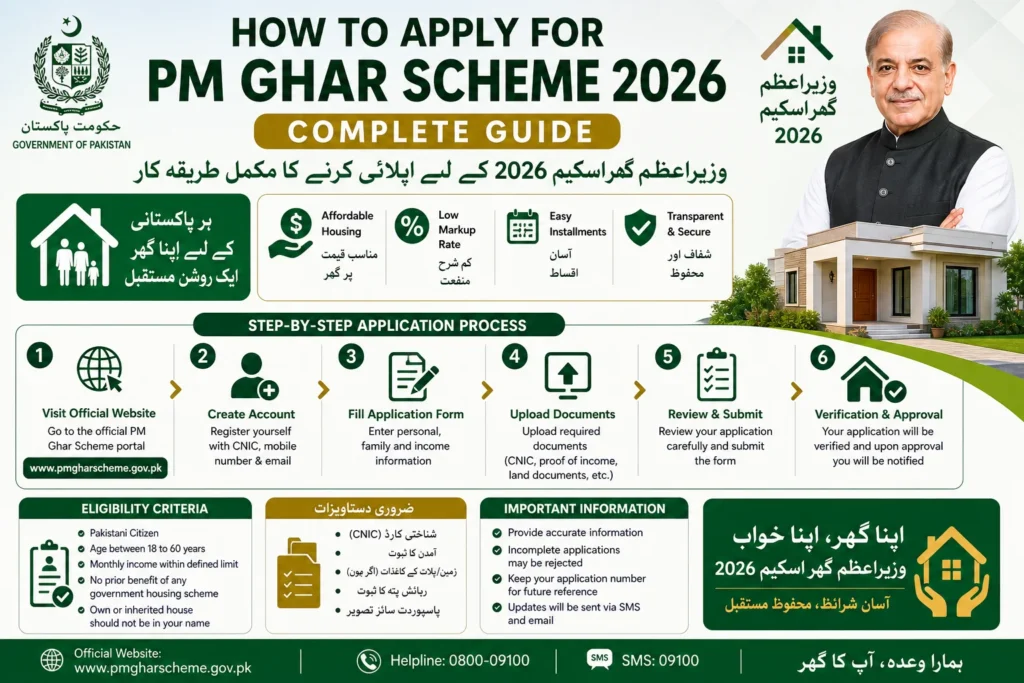

Applying for the Apna Ghar Program has been streamlined to facilitate ease of access. Interested individuals can typically initiate their application through the designated PFIs. Many banks have also launched online portals, such as the application form available on Bank AlFalah’s website, allowing applicants to apply digitally. This digital approach enhances efficiency and convenience for potential homeowners.

Impact and Future Prospects of the Ghar Hoto Apna Initiative

The long-term impact of the Ghar Hoto Apna initiative is expected to be profound, significantly contributing to social uplift and economic development. By enabling citizens to own homes, the program fosters a sense of security and stability, leading to improved living standards and stronger communities. It also serves as a potent stimulus for the construction sector, generating employment opportunities and driving economic growth. This visionary program holds the promise of transforming the housing landscape in the country for years to come.

Conclusion

The Prime Minister Apna Ghar Program: Ghar Hoto Apna stands as a beacon of hope for countless citizens aspiring to own a home. With its generous markup subsidy, flexible loan options, and robust risk-sharing mechanism, the program effectively removes significant barriers to affordable housing. By fostering homeownership and stimulating economic activity, it is poised to create a lasting positive impact on the nation, fulfilling the dream of “Ghar Hoto Apna” for many.

Frequently Asked Questions (FAQs)

1. What is the “Prime Minister Apna Ghar Program: Ghar Hoto Apna”?

The “Prime Minister Apna Ghar Program” is a federal government initiative offering a Markup Subsidy and Risk Sharing Scheme to provide affordable housing finance. It helps eligible citizens purchase or construct their first homes with subsidized fixed markup rates.

2. Who is eligible to apply for the “Apna Ghar Program”?

The scheme is open to Pakistani citizens holding CNICs who are first-time homeowners and do not currently own any housing unit in their name.

3. What types of housing units does the “Ghar Hoto Apna” scheme cover?

The scheme covers the purchase of houses/flats, construction of a house on an already owned plot, or the purchase of a plot for subsequent construction of a house.

4. What is the maximum loan size and tenure under the “Wazir-e-Azam Apna Ghar Program”?

Applicants can avail a maximum loan of up to PKR 10 million. The loans are available for a tenor of up to 20 years, with the government providing a markup subsidy for the first 10 years.

5. How much is the fixed markup rate for customers under the “Apna Ghar Program”?

Customers benefit from a flat fixed markup rate of 5 percent. The government covers the remaining markup difference with the bank’s rate (One Year KIBOR + 3%).

6. Are there any processing fees or prepayment penalties for loans under this program?

No, a key feature of the “Apna Ghar Program” is that no processing costs or prepayment penalties will be charged to customers, making the financing more accessible and transparent.

7. Which financial institutions are participating in the “Ghar Hoto Apna” initiative?

All commercial banks, Islamic banks, Microfinance Banks (MFBs), and the House Building Finance Company Limited (HBFCL) are designated as Participating Financial Institutions (PFIs).